Originally published in March 2025, this guide has been fully updated for 2026 to reflect the latest best practices, tools, and real-world insights shaping how modern accounting firms approach time tracking and billing.

Most accounting firm leaders know the feeling: the team is working long hours, the WIP report is bursting, but at times the bank balance doesn’t seem to reflect the effort. Revenue leakage — billable work that never makes it onto an invoice or onto the books at full value — is a common drain on firm profitability.

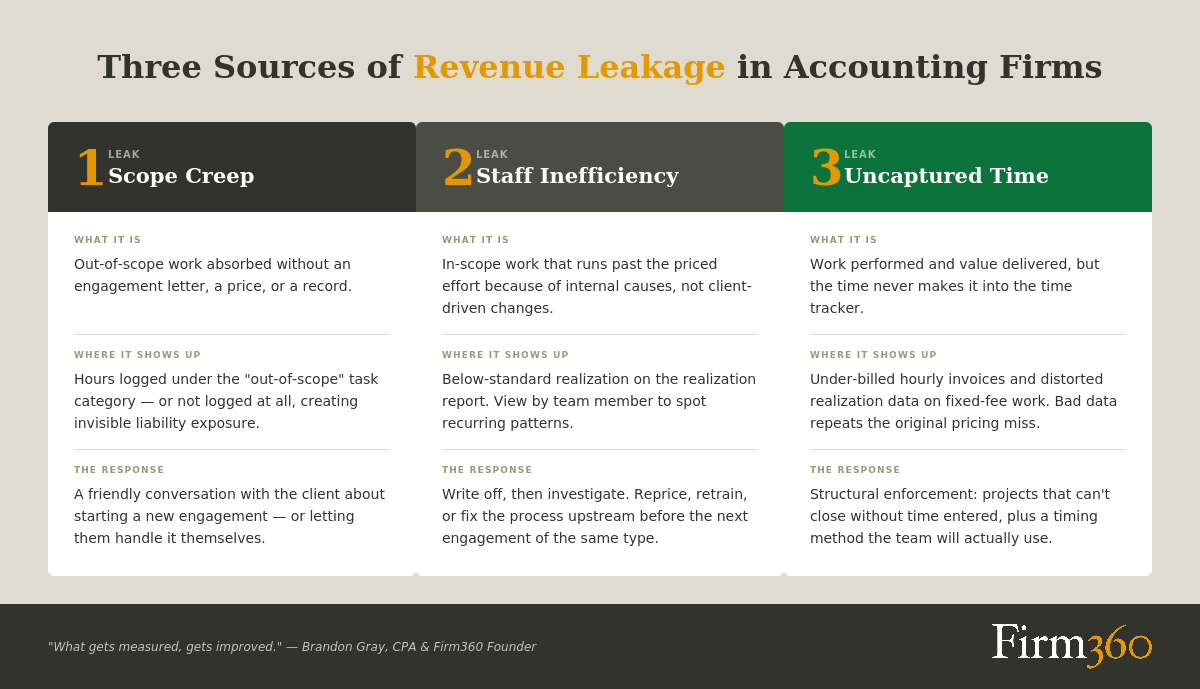

For small and mid-sized firms, three sources typically account for most of that leakage. The first is scope creep: out-of-scope work absorbed without an engagement letter, a price, or a record. The second is staff inefficiency: in-scope work that takes longer than the engagement was priced for, with the cause being internal rather than client-driven. The third is uncaptured time: work that staff perform but never log, which under-bills hourly engagements outright and distorts the realization data on fixed-fee work. The cure for the third is also what makes the first two visible — accurate, consistent time capture across every engagement.

This guide walks through strategies that CPA (and Firm360 founder) Brandon Gray uses to catch and contain leakage sources: engagement-letter discipline, time tracking that makes out-of-scope and over-budget work visible, the reports that surface them, the review process that diagnoses cause and chooses response, and the cultural levers that reinforce it all. For a wider operations view of the firm, the Firm360 practice management guide is a useful next read.

Leak #1: Scope Creep — the Dominant Leak, and a Liability Exposure Too

Scope creep is problematic for a couple of reasons, Gray explains:

“Scope creep is probably the biggest risk for a small firm — not only from a revenue leakage perspective, but from a professional liability perspective if the out-of-scope service isn’t covered in your engagement letter.”

— Brandon Gray, CPA & Firm360 Founder

The white-glove service offered by many firms means that clients may feel comfortable reaching out for assistance on most anything that involves finances.

“Accounting firms work hard to provide a high level of service and you often become your clients’ trusted advisor. They ask for help with things like FAFSA forms, lease review, and more. Generally these are out of scope, but most firms just say, ‘Sure, send it over and I’ll help.’”

— Brandon Gray, CPA & Firm360 Founder

Two things to hold onto. First, some scope creep is normal. The goal is to keep it from turning into a write-off or a liability problem. As Gray explains, “It’s normal to have a certain amount of work that’s out-of-scope, but you don’t want it to become material.”

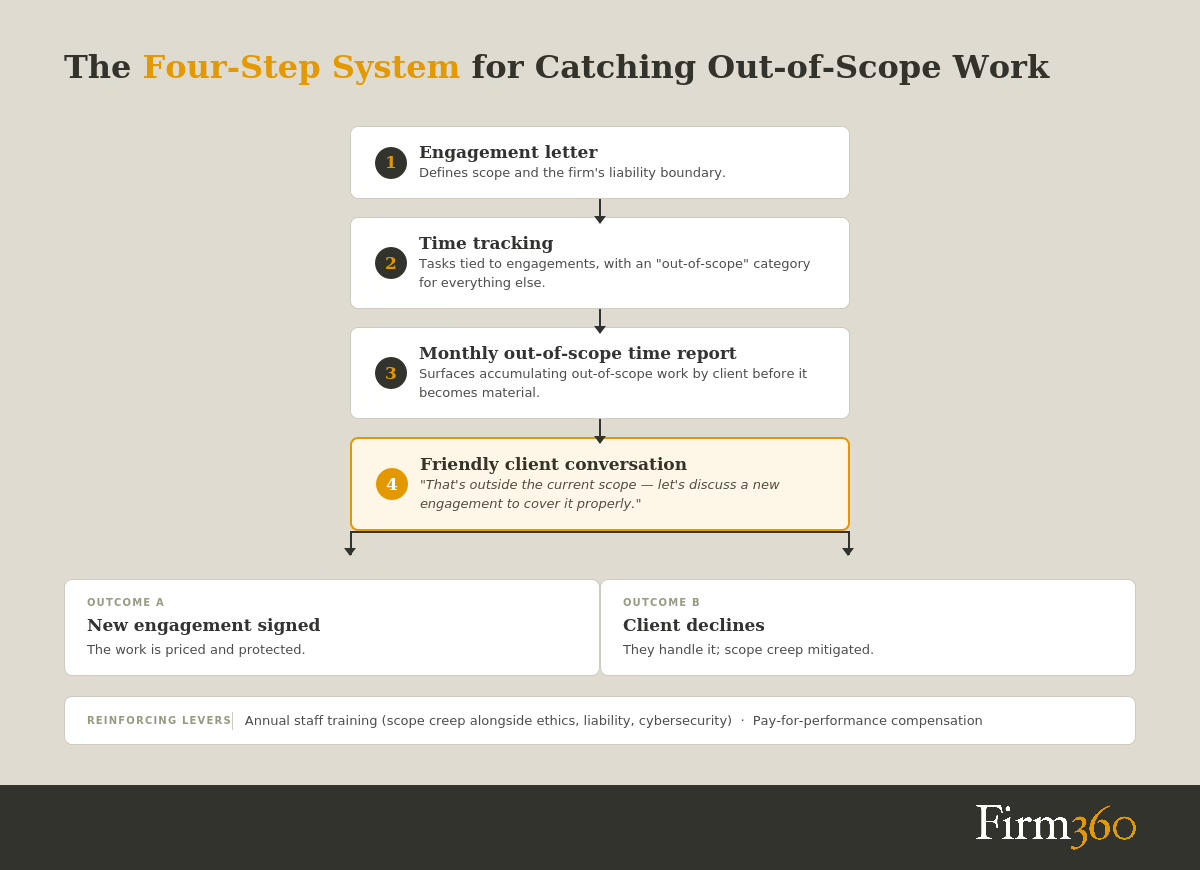

Second, the engagement letter is both the firm’s scope boundary and its liability boundary. Work performed outside of an engagement letter exposes the firm on two fronts at once.

The cure for both problems is the same: make out-of-scope work visible.

Leak #2: Staff Inefficiency

When in-scope work takes longer than the engagement was priced for and the cause is not scope expansion, the firm has an internal problem rather than a client problem. The solution is relative to the cause: If it’s not the client’s fault, then it’s probably best to write it off, particularly if it’s not a material amount.

The risk is treating that write-off as the end of the story. A single engagement running over by an immaterial amount can reasonably be absorbed. Recurring inefficiency-driven write-offs — the same engagement type, season after season, sometimes the same staff member — are something different. They are revenue leakage that compounds quietly because each instance looks small.

The realization report surfaces the pattern. Break it down by team member to see which team members are profitable — an angle that distinguishes engagement-level pricing problems from team-level capacity or skill problems. Treating the realization report as a diagnostic is what turns the write-off into actionable information rather than a recurring cost.

The same materiality standard Gray applies to scope creep applies here: A small amount of inefficiency-driven write-off is normal. A material amount — or a small amount that recurs in the same place — is a signal to investigate the underlying cause and address it before the next engagement of the same type, whether that means repricing the work, retraining or restaffing the team, or fixing a process bottleneck upstream of the engagement.

Leak #3: Uncaptured Time

The simplest leak is also the most direct: work is performed, value is delivered to the client, and the time never makes it into the time tracker. For hourly engagements, the invoice is lower than it should have been. For fixed-fee engagements, the leakage is harder to see but no less real: the realization report cannot tell you which engagements are truly profitable, because the effort it shows is understated. Pricing decisions made on bad data tend to repeat the original miss.

Gray’s solution is structural rather than behavioral:

“If you set up projects so that they cannot be completed without time, the time will be entered. Some firms choose to use start/stop timers, but many simply opt to allow time entry at the end of a specific task.”

— Brandon Gray, CPA & Firm360 Founder

The point is to take the friction out of compliance. Asking staff to track time mentally at the end of a long day, or to reconstruct a week from memory on Friday afternoon, produces missed entries and estimates that miss real effort. Tying task completion to time entry shifts compliance from staff diligence to system enforcement. The choice between start/stop timers and end-of-task entry is a matter of team preference; what matters is that the workflow makes time entry the path of least resistance.

The downstream effect of this control is what makes the rest of the system work. The realization report, the out-of-scope time report, and the review process all assume the underlying time data is complete. When time is captured systematically, the reports surface real signals and the firm can act on them. When time is captured unevenly, every report is a guess.

Time Tracking That Makes Leakage Visible

Gray’s controlling principle: “What gets measured, gets improved.” Accurate time tracking is key. Set up time tracking so that it’s tied only to tasks that are included in an engagement, or to an ‘out-of-scope’ task, so it becomes visible.

The standard has three elements.

Tasks tied to engagements, plus an “out-of-scope” category. Every task in the time tracker maps either to an engagement deliverable or to the “out-of-scope” bucket. There is no other place for time to land. Out-of-scope hours show up in a highly visible way; in-scope hours roll into the realization report, where engagements running past their priced effort surface as below-standard realization. Both leakage sources — scope creep and internal inefficiency — become visible through the same data.

Projects that cannot close without time. If you set up projects so that the related tasks cannot be completed without time, the time will be entered. The system does the enforcement.

A timing method the team will actually use. Whether your firm uses timers or simply prompts staff to enter time at the end of a specific task, the right method is the one that produces consistent entries.

The same discipline applies to flat-rate work. If you’re billing at a flat rate, then you need to be capturing the out-of-scope work through project tracking. The time captured in this scenario is not for the current invoice, but can impact the next pricing or staffing conversation.

Reports That Surface Revenue Leaks

Gray relies on two primary reports for catching leakage, with a third for after-billing visibility.

The out-of-scope time report — run monthly. Gray names the office administrator as the owner: “The office administrator can run the out-of-scope time report monthly. Also, keep an eye on the realization report. Out-of-scope activities will be noticeable there.” This is the early-warning system. When out-of-scope hours start trending up for a particular client, a conversation needs to happen with the client about whether they’d like to start a new engagement.

The realization report — annually for most firms. “For us it makes the most sense to look at the client realization report annually, but you can run it by month if you prefer. Monthly review can be particularly helpful during periods when you’re onboarding new billing staff.” Run it by revenue and by team member to see who is profitable.

The payment report — after billing. Gray points to two checkpoints for write-off visibility: “You can look at write-offs before billing, or after billing. Before billing, the write-offs will be evident through the realization report. After billing you can run a payment report.” Write-off ownership is a firm-by-firm choice. Gray notes that write-offs “are tracked only by partners in some firms, also by the office manager in others.”

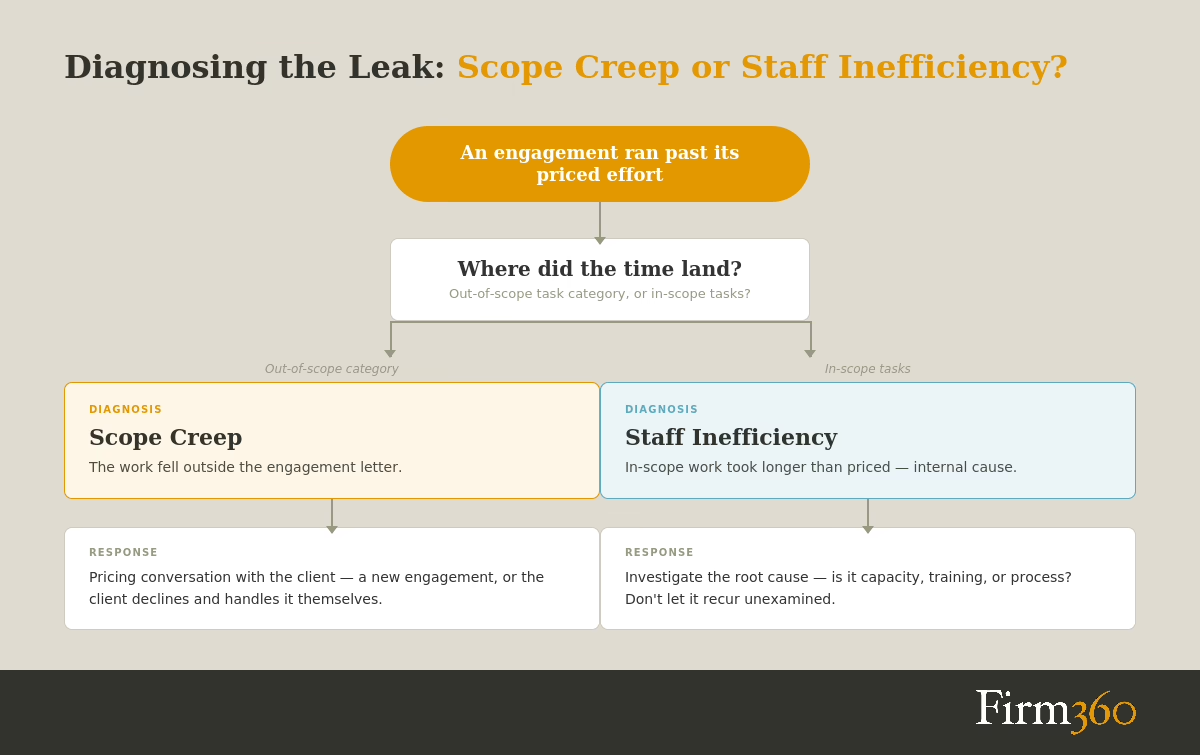

The Review Process: Diagnose the Cause, Choose the Response

Both leakage sources show up on the realization report: an engagement eats more time than it was priced for. What separates them — and what determines the response — is diagnosing why.

“If we see during review that too much time was spent on that month’s work, we look to see if it went out of scope. If so, we may adjust the pricing after a discussion with the client. If it’s not the client’s fault, then we may write it off, depending on whether it’s a material amount.”

— Brandon Gray, CPA & Firm360 Founder

The diagnostic comes from looking at where the time landed. Hours under the “out-of-scope” task category point to scope creep, and the response is a pricing conversation with the client, ideally formalized as an engagement addendum. Hours under in-scope tasks that still pushed the engagement past its priced effort point to internal inefficiency, and the response is the write-off-and-investigate logic from the previous section.

In both cases, the partners should not typically be a bottleneck for invoicing. Gray’s firm trains the billing manager into partner-level judgment within a clear box of authority: “We train the billing manager to think the way partners think about billing, providing them a clear box within which they can make their own judgement. We encourage them to take ownership as the biller to be profitable, telling them, ‘when in doubt, bill it.’” Most invoices ship without partner intervention; exceptions — material write-downs, scope conversations, new clients — escalate.

Handling Out-of-Scope Requests in Real Time

Reports tell the firm where scope creep is happening. The conversation in the moment is what prevents it from becoming material.

“There’s a saying, ‘good fences make good neighbors,’ that’s appropriate here. Make sure you outline and discuss scope clearly with your clients before engagements begin. If out-of-scope requests come up, have a friendly conversation about creating a new engagement for that work.”

— Brandon Gray, CPA & Firm360 Founder

The dynamic often resolves itself: The client may opt to take care of the request themselves when they realize they’ll need to pay for it, or they may opt to sign an additional engagement. Either outcome protects the firm — and the relationship — better than absorbing the work silently.

Cultural and Structural Levers

Two practices can reinforce the system at the firm level.

Annual staff education that includes scope creep. A company culture that addresses scope creep proactively through training sets itself up for success:

“In our firm we conduct annual education for staff around things like confidentiality, ethics, liability and risk, and cybersecurity. Scope creep is part of that conversation.”

— Brandon Gray, CPA & Firm360 Founder

That framing helps change how staff respond when a client asks for an out-of-scope favor.

Compensation as a behavioral lever. Some firms are transitioning to a “pay for performance method,” in which case staff normally keep the out-of-scope work to a minimum because they know they won’t get compensation for it. When compensation rewards realized revenue, scope creep becomes self-correcting.

How Time Tracking and Billing Software Supports

Some of the concepts above work with spreadsheets; others require software and automation to work at scale. The Firm360 time tracking and billing module supports the controls in this article. Whichever platform you choose, look for capabilities like these.

- Capture more billable time through timers and task-linked entry.

- Quickly improve realization by spotting scope creep before work turns into write-offs.

- Reduce billing errors and disputes with consistent, audit-ready time detail.

- Support accurate and timely billing with workflow automation features that ensure the right person is reviewing and issuing invoices within expected timelines.

- Support fixed-fee and recurring services by tracking effort and margin trends without hourly billing.

- Simplify write-off analysis. See what was written down, why, and which clients are driving it.

Conclusion

You don’t need to rebuild the entire billing system to start closing leaks. Pick two changes and run them for the next three months. A pragmatic starter pair: add an “out-of-scope” task category to your time tracker, and have the office administrator run the out-of-scope time report monthly. Those two changes alone make scope creep visible and give the firm a chance to act before the engagement letter, the price, or the client relationship gets stretched.

To see how these controls fit alongside the rest of firm operations, the Firm360 practice management guide is a natural next stop.

FAQs

What causes revenue leakage in accounting firms?

For small and mid-sized firms, three causes account for most of it: scope creep (out-of-scope work performed without an engagement letter or agreed-upon price), staff inefficiency (in-scope work that runs past the priced effort because of internal causes), and uncaptured time (work performed but never logged, leading to under-billing on hourly engagements and distorted realization data on fixed-fee work).

How can you tell scope creep apart from staff inefficiency?

Both show up the same way — an engagement runs past the time it was priced for. The diagnostic comes from looking at where the time was spent. If hours landed under the “out-of-scope” task category, the cause is scope creep and the response is an engagement conversation. If hours landed under in-scope tasks but the engagement still ran over, the cause is internal — pricing, capacity, training, or process.

Should accounting firms track time if they use fixed-fee pricing?

Yes. If you’re billing flat rate, then you need to be capturing the out-of-scope work through project tracking. Time data on fixed-fee work is not for the client invoice — it is for the realization report and the next pricing conversation.

What is the best billing cadence for recurring engagements?

Recurring fixed-fee engagements should bill automatically on a defined schedule. The discipline is in the exception review afterward: when the hours run hot, diagnose whether it was scope creep or the firm’s own delivery, then act — adjust pricing with the client, or write off depending on materiality.

How do you reduce write-offs without upsetting clients?

Communication is key. Alert clients when requests are out-of-scope, giving them the option to continue under a new engagement, or to handle it in another way.

What reports should we run to find revenue leaks?

The out-of-scope time report, the realization report, and the payment report.

How do you standardize time entries across staff?

Three things make the difference: tie tasks to engagements (with an “out-of-scope” category for everything else), set projects so they cannot be completed without time entered, and pick a timing method — start/stop timers or end-of-task entry — that the team will actually use. Reinforce through annual staff education.

Expert Bio

Brandon Gray is a CPA, founding member of Banks, Gray & Crumpler, PLLC in Goldsboro, NC, and a Master of Science in Accounting graduate of East Carolina University. After years of battling clunky legacy systems in his own practice, he co-founded Firm360, a cloud-based practice management platform — giving him a front-row seat to hundreds of firms streamlining their operations. He was named one of CPA Practice Advisor’s “20 Under 40” Top Influencers in 2022. Brandon also facilitates C12 Christian CEO coaching groups in Eastern NC, serves as Assistant Chief for the New Hope Volunteer Fire Department, is a private pilot, and an avid outdoorsman with his children.